Press release 29 July 2021

Products

Product pages available in

EN - DE - FR - ES

Sustainability

Climate action progress

XCarb™ - towards net zero steel

Steel and the circular economy

Smart carbon technology

Clean power steelmaking

Circular carbon steelmaking

Capture and storage of fossil fuel carbon

Commitment to ResponsibleSteel™

Life cycle assessment

Recycling advanced steels

Our automotive outcomes

News, events and stories

Highlights of ArcelorMittal's second group climate action report:

- Targeting 25% group-wide global carbon-emissions reduction by 2030

- Estimated cost of ca. $10 billion

- Europe 2030 target increased to 35%

- ArcelorMittal Sestao to become world’s first full-scale zero carbon-emissions plant

- New collaboration announced with Science Based Targets initiative - Targets to be linked to executive remuneration

ArcelorMittal (‘the Company’) has today published its second group climate action report, following the first group report published in May 2019 and the European climate action report published in May 2020.

In the new report, ArcelorMittal has for the first time announced a 2030 global carbon emissions intensity reduction target of 25%. It has also increased its European 2030 carbon emissions intensity reduction target to 35% from 30% previously announced. All targets are on a scope 1 and 2 basis. The Company had previously announced a net zero by 2050 ambition in September 2020.

The Company’s targets are underpinned by a set of assumptions:

- The cost of green hydrogen will become increasingly competitive over the next decade but will still require government support.

- Carbon capture, utilisation and storage (CCUS) infrastructure will take time to be built at scale. While Europe is expected to take the lead, CCUS infrastructure has the potential to expand quickly in the US and Canada – providing some potential upside to our assumptions.

- Different regions of the world will continue to move at very different paces and the level of climate ambition will differ between jurisdictions at any given time.

- The introduction of climate-friendly policies in other regions will be 5–10 years behind Europe.

Reflecting these assumptions, each region in which the Company operates is designated as either ‘Accelerate’ (supported by the introduction of more ambitious climate change policy) or ‘Move’ (reflecting a policy environment not yet providing any meaningful support to accelerate steel industry decarbonization and where accelerating without supportive policy will render the asset uncompetitive versus national/regional competition).

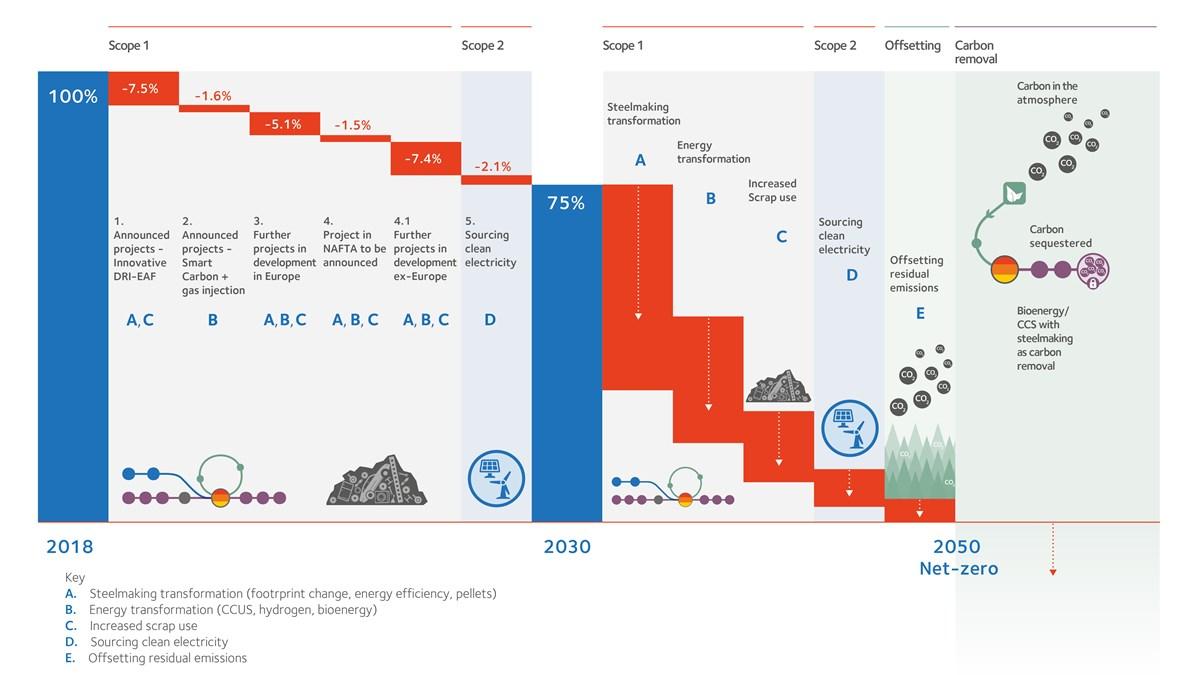

2030 target breakdown and capex

The new climate action report provides a roadmap that illustrates the Company’s current thinking on the journey to net zero steelmaking. Five key levers are identified as the stepping-stones to achieve net zero by 2050. These are:

A – Steelmaking transformation: In the course of the coming decades the steel industry will undergo a transformation of the assets used to make steel on a scale not seen for over 100 years. This includes in a first phase the transition from coal (in the blast furnace) to natural gas (in a DRI plant) as a precursor to green hydrogen DRI.

B – Energy transformation: The energy used to make steel in future years will undergo a further and more radical transition, from high-emitting fossil fuel-based energy to low and zero-carbon emissions forms of energy. This includes green hydrogen, circular forms of carbon and CCUS technologies.

C – Increased use of scrap: As well as using scrap in the EAF, we will increase the use of scrap in blast furnace-basic oxygen furnace (BF-BOF) steelmaking.

D – Sourcing clean electricity: We will focus on increasing the amount of low and zero-carbon emissions electricity we consume. We plan to do this by purchasing renewable energy certificates and by direct power purchase agreements (PPA) with suppliers from renewable projects.

E – Offsetting residual emissions: There are likely to remain residual emissions for which either there is no feasible technological solution or the solution involves excessively high economic or social costs. For these emissions ArcelorMittal will buy high-quality offsets or launch projects to generate high-quality carbon credits.

Further specific detail for the 2030 target is provided aligning with these five levers, as follows:

|

1- |

Announced projects Innovative DRI-EAF |

-7.5% |

A, C |

|

2- |

Announced projects Smart Carbon and gas injection |

-1.6% |

B |

|

3- |

Further projects in development in Europe |

-5.1% |

A, B, C |

|

4- |

Project in NAFTA to be announced |

-1.5% |

A, B, C |

|

4- |

Further projects in development ex-Europe |

-7.4% |

A, B, C |

|

5- |

Sourcing clean electricity |

-2.1% |

D |

To achieve this reduction the Company has estimated it will require a gross investment of c. $10 billion of capital expenditure. The Company expects to deploy approximately 35% of this c. $10 billion investment by 2025 with the remainder in the second part of this decade.

Over time, and with the deployment of appropriate technologies, it is expected that low-carbon steel-making technologies will become more competitive than higher-carbon steel-making technologies. However, this is not the case today and therefore companies will need support through well-designed policy to help moderate the initial capital costs, which will not yield a reasonable EBITDA return in the short-to-medium term, as well as the higher opex costs in the transition period that could otherwise render them uncompetitive. ArcelorMittal believes support of approximately 50% of total costs will be needed to enable companies to remain competitive regionally and globally through the transition period.

In terms of our investment decision-making, each major capex project proposal is required to demonstrate its CO2 impact to our Investment Allocation Committee (IAC). The IAC considers both the potential future carbon cost as well as the capital cost of decarbonization, to maximize our chances of achieving our targets while ensuring each project is economically justifiable and earns its cost of capital.

The announced Innovative DRI-EAF projects include:

- Reducing emissions in Spain by 50% by constructing a 2.3 million tonne hydrogen-powered DRI unit at Gijon, as well as a new hybrid EAF. The construction of these units will transition the Gijon plant away from BF-BOF steelmaking to DRI-EAF production.

- Transforming ArcelorMittal Sestao to be the world’s first full-scale zero carbon-emissions steel plant by 2025. 1 million tonnes of DRI will be transported by rail from Gijon to Sestao to be used as feedstock for its two EAFs. Sestao will also change its metallic input; power all steelmaking assets with renewable electricity; introduce new emerging technologies that will replace the remaining use of fossil fuels in the steelmaking process with carbon-neutral energy inputs.

- Plans to build a large-scale industrial plant for DRI and EAF-based steelmaking in Bremen, as well as an innovative DRI plant and EAF in Eisenhuttenstadt. CO2 savings of up to more than 5 million tonnes could be possible depending on the availability of green hydrogen.

- The construction of a DRI plant in Dunkirk to produce 2 million tonnes per year of hot metal, reducing CO2 emissions by 2.85 million tonnes by 2030.

- Testing of hydrogen injection at our DRI facility in Quebec. The test will start with a limited injection of 5% within the energy mix and further phases are planned in the future. Renewable sources – specifically hydroelectric – provide 99% of Quebec’s energy.

The announced Smart Carbon projects include:

- Torero and Carbalyst – two technologies to enable the use of circular carbon, which does not add carbon to the biosphere. Torero is a torrefaction process to make steel-specific bioenergy from waste wood and waste plastic. Carbalyst allows us to use steelmaking waste gases to produce basic chemicals such as bio-ethanol, which are the key building blocks of plastics.

- In Gent, we are constructing an industrial-scale demonstration plant that converts waste wood into bio-coal through torrefaction. Two reactors will each produce 40,000 tonnes of bio-coal annually that can be used in the blast furnace as a substitute for coal. Reactor 1 is expected to start production in 2022 and reactor 2 in 2024.

- In Gent we are also constructing an industrial scale Steelanol demonstration plant to capture carbon off-gases from the blast furnace and convert them into bioethanol using microbes. The plant is expected to be completed in 2022 and will produce 80 million litres of bioethanol annually.

ArcelorMittal continues to believe that both technology pathways (Innovative DRI and Smart Carbon) have an important role to play in helping the steel industry, and the global economy, achieve net zero by 2050. Furthermore, the Company continues to develop a third route, direct electrolysis, which is still in the research and development phase. Which specific routes will ultimately be adopted is likely to differ from region to region and depend on policy choices and the availability of government funding. The Company has been able to accelerate plans for the world’s first zero carbon-emission steel plant in Spain for example because of government policy to accelerate the availability of green hydrogen.

Policy

The Company has also outlined in the report the combination of policy instruments it believes will be required to address not just the significant capital expenditure to transition to the new zero carbon-emissions technologies, but also the considerably higher operating costs associated with these technologies at least in the short-medium term until low and zero carbon-emission technologies become competitive. Policy instruments such as contracts for difference, used so effectively in enabling the renewable energy industry to become competitive, will play an important role in ensuring a level playing field during the transition period.

ArcelorMittal intends to actively and directly engage with policymakers and organisations that advocate for the policies and conditions that will enable steel to accelerate and achieve its net-zero transition globally while remaining competitive.

Science based targets

The Company has also announced a new collaboration with the Science Based Target initiative (SBTi) and a commitment to publish a science-based target within the next two years. The collaboration will support the SBTi to develop a new science-based methodology for the steel sector.

As part of the Net Zero Steel Pathway Methodology Project (NZSPMP), ArcelorMittal has, with other steelmakers, been working on a set of principles by which it believes the steel industry’s alignment with a net zero by 2050 outcome should be measured. These principles were published on 27 July.

Just transition

ArcelorMittal is aware of key stakeholder concerns around a just transition. We are seeking to employ best practice principles to understand the social impact of our decarbonization strategy and support engagement with our key stakeholders and collaborate with policy makers in addressing this issue.

TCFD and Climate Action 100+ Net Zero Benchmark Alignment

The Company has followed the TCFD guidelines and the Climate Action 100 Net Zero benchmark. While we have not yet achieved full disclosure according to either the TCFD or CA100 Net Zero benchmark, we believe this report marks a meaningful step forward, thereby demonstrating to stakeholders our commitment to adopting a leadership position in the decarbonization of the steel industry in terms of target-setting, performance and disclosure.

Executive remuneration

The Company now intends to link these targets to executive remuneration. Details will be published in due course.

“As the world’s most prolific material, steel can make a huge contribution to the decarbonization of the global economy. Steel is already the material of choice due to its lower carbon footprint and high recyclability. But we can and must go further as zero carbon-emissions steel has the potential to be the backbone of the buildings, infrastructure, industry and machinery, and transport systems that will enable governments, customers and investors to meet their net-zero commitments.

“ArcelorMittal has been working hard to be at the forefront of our sector in the net-zero transition, as we believe not only will this help decarbonize the global economy but will also generate opportunities in multiple aspects of our business.

“This is reflected in the new targets we have announced today. We have for the first time published a group target for 2030, alongside a more ambitious target for our European business. These targets we believe are aligned with our net zero 2050 ambition and we have also announced today a new collaboration with the Science Based Target initiative.

“These targets reflect the uneven pace of change that is the reality of the world’s decarbonization journey. In regions of the world like Europe, where we are observing an ‘Accelerate’ policy scenario, we can be more ambitious – with plans to reduce emissions by 35% within the next decade. In other markets we face a situation where being a first mover will result in us being uncompetitive in that market. For our target setting today we assume progress in other regions of the world will be at least five years behind Europe.

“With COP26 focused on addressing the acceleration that is critical in the next decade if the world is to reach its 2050 target, it may be that we will see a swifter evolution of this policy environment than is currently envisaged. Policymaking has a catalytic role to play. ArcelorMittal intends to step up our advocacy for policies that support the acceleration of this transition, addressing the fact that both capex and opex costs will be significantly higher, at least in the short to medium term.

“Ultimately the goal is to ensure that the technologies that will decarbonize the steel-making process are competitive. The good news is that we already have two technology routes - Innovative DRI and Smart Carbon - which can enable the decarbonization of the industry with a third, direct electrolysis, looking encouraging. Given our global profile we believe it is sensible to continue to develop both these technology routes which essentially encompass the clean energy routes of both green hydrogen and also bio-energy with carbon capture utilization and storage.

“In Europe our strategy is largely focused on the Innovative DRI pathway. This reflects the commitment in Europe to prioritize the availability of green hydrogen at competitive prices. Spain’s plan to accelerate the availability of renewable energy and green hydrogen underpins our recent announcement that ArcelorMittal Sestao will become the world’s first full-scale zero carbon-emissions steel plant.

“In many respects the challenges confronting steelmaking today resemble those faced by renewable energy over a decade ago. The importance of solar and wind was widely acknowledged yet the technology remained economically prohibitive. Targeted, reliable and thoughtful policies supported innovation and investment that enabled both companies and their financing partners to make long-term planning decisions.

“We are optimistic that the same will happen in steel. It is too critical a material on so many levels for that not to be the case. And as developing economies continue to grow, the world will need more steel, not less, to give a better quality of life to billions of people.

“Over this past year, we have engaged with our stakeholders on climate more than ever before. I hope this report demonstrates how seriously we take your input, how closely we have listened to your questions, and how committed we are to providing solutions."

Aditya Mittal, CEO ArcelorMittal

You may also be interested in

Who we are

Your co-engineering partner Your global steel solution providerOur purpose: Smarter steels for people and planetInteractive mapInnovation

The future of steelGlobal R&DInnovation in practiceFast Lane: ArcelorMittal’s sampling and pre-serial production serviceCustomer statementsLatest customer casesS-in motion® solutions

3D car configuratorBattery electric vehicles Battery pack for BEVChassisFront chassis for EVsRear Chassis for BEVsPickup trucksMid-size Sedan and SUVC-segment vehicles Light commercial vehicles Commercial trucksFront seatsSustainability

Climate action progressXCarb™ - towards net zero steelSteel and the circular economy Smart carbon technologyClean power steelmakingCircular carbon steelmakingCapture and storage of fossil fuel carbonCommitment to ResponsibleSteel™ Life cycle assessmentRecycling advanced steelsOur automotive outcomesTailor your ArcelorMittal Automotive web experience

My ArcelorMittal Automotive space

This is your personal space on ArcelorMittal's global automotive website. You can keep your favorite ArcelorMittal automotive web pages and documents in a safe place

My spaceConfigure this website

If you want, you can tailor your web experience on this automotive website to your personal needs. By selecting your job profile and/or region (both optional) you enable us to personalize the content you see on this website.

No matter which job profile or region you select, you will always have unlimited access to all the information on this website. The only thing that changes is that you will be offered more tailored content. As well as your profile and region, we also use your browsing history on this website to remember your personal preferences and identify the most appropriate content for you.

We are confident that this will help you to find the inspiration you are looking for on the ArcelorMittal automotive website.